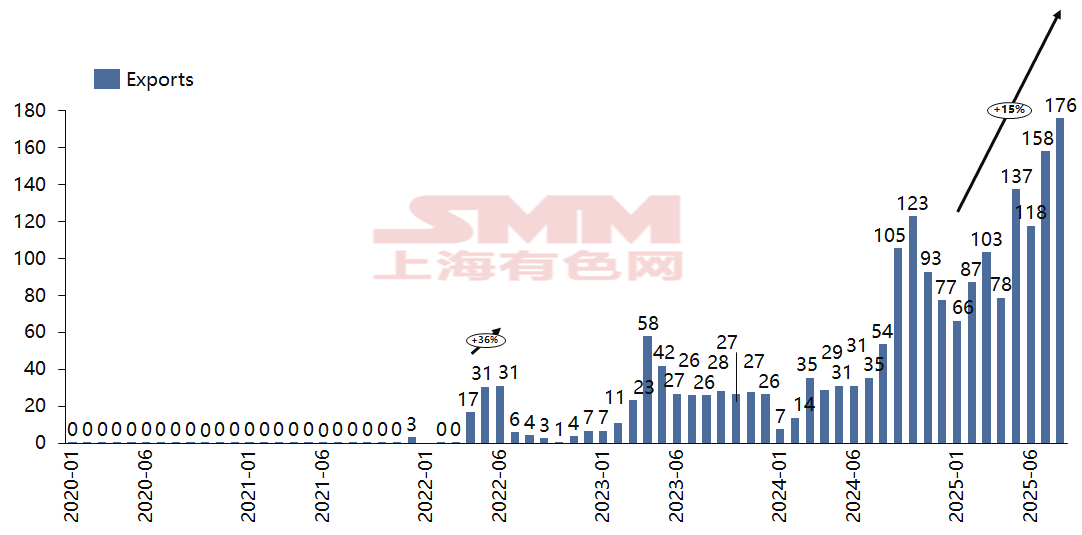

■ Steel Billet Export Volume Multiplies

Before 2022, China's annual steel billet exports were less than 100,000 mt. By 2022, the total annual export volume surged over a thousandfold YoY to 1.0269 million mt, with the most significant exports occurring in Q2. This was primarily due to the Russia-Ukraine conflict, which reduced international billet supply, pushed prices in some countries to historic highs, and led China to resume its billet export business.

Figure 1: China's Monthly Steel Billet Exports, 2021-August 2025 (10,000 mt)

Data source: General Administration of Customs

From 2024 to 2025, China's billet exports reached new heights. The total export volume for 2024 was 6.3439 million mt, up 93.42% YoY. According to data from the General Administration of Customs, China exported 1.76 million mt of steel billets in August 2025, up 12% MoM and 230% YoY. Cumulative billet exports from January to August 2025 reached 9.24 million mt, up 292% YoY, making it imminent to surpass the 10 million mt mark within the year. The surge in data over the past two years is mainly attributed to a strong international protectionist backlash against the excessive growth of China's steel exports. In 2024, the Chinese steel industry faced over 90 anti-dumping cases, primarily involving cold-rolled and hot-rolled sheet and plate products. Semi-finished products like steel billets faced relatively fewer anti-dumping measures, providing new opportunities for domestic export traders.

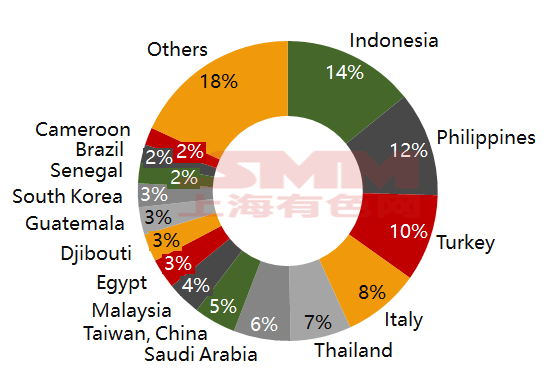

■ Southeast Asia and Middle East Are Primary Destinations for China's Steel Billet Exports

Figure 2: Regional Distribution of China's Steel Billet Exports, January-August 2025

Data source: General Administration of Customs

In terms of export destinations, the top 10 destinations for China's steel billet exports from January to August 2025 were Indonesia, the Philippines, Turkey, Italy, Thailand, Saudi Arabia, Taiwan China, Malaysia, Egypt, and Djibouti. Notably, Malaysia rose from 27th place last year to 8th this year, with export data only appearing in November-December last year.

Southeast Asia and the Middle East have become major destinations for China's billet exports, driven by strong growth in infrastructure construction demand in these emerging markets. However, local steel rolling capacity is relatively insufficient, leading to a surge in demand for imported billets. Chinese billets quickly filled this supply gap due to their price advantage. Meanwhile, some Chinese-funded steel mills in ASEAN countries used Chinese billets to shorten the smelting and rolling processes, reducing the use of imported iron ore, effectively substituting Australian and Brazilian iron ore with Chinese billets.

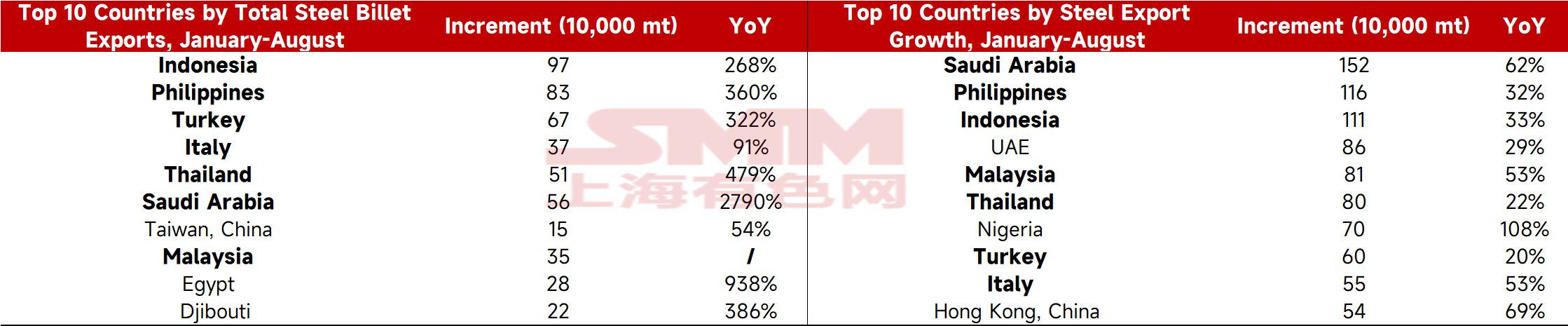

Table 1: Comparison of Total Steel Billet Exports and Total Steel Product Exports, 2025

Data source: General Administration of Customs

An interesting observation is that, from January to August 2025, seven countries overlapped between the top 10 destinations by YoY growth for China's steel product exports and the top 10 destinations for billet exports. The top 10 billet export destinations all saw significant YoY increases, with Saudi Arabia's increase exceeding a thousandfold.

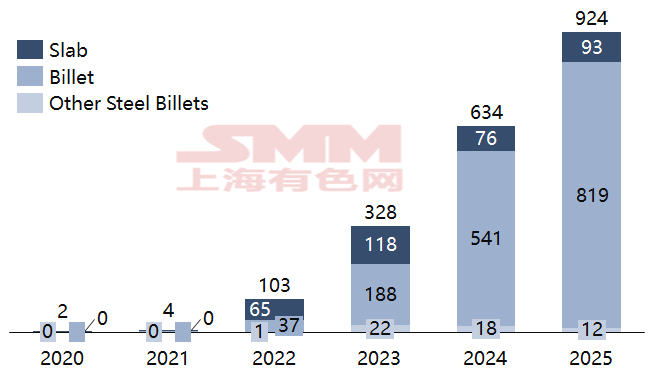

■ Since 2023, Billets Have Surpassed Slabs as the Primary Steel Billet Export Variety

Figure 3: Variety Breakdown of China's Steel Billet Exports, 2020-August 2025

Data source: General Administration of Customs

Customs data show that before 2022, slab and billet export volumes were comparable, with slab exports even slightly higher in 2022. The situation changed from 2023 onwards, as billet export volume surpassed that of slabs. From January to August 2025, slab exports totaled 930,000 mt, accounting for 10.07%, while billet exports reached 8.19 million mt, accounting for 88.65%. Other steel billet exports totaled 117,500 mt, accounting for 1.27%.

Weak domestic long product demand was a necessary condition for the significant growth in billet exports. persistently sluggish end-use demand from sectors like real estate led to continuously weak profitability for long products (e.g., rebar, sections). Since last October, the price spread advantage of rebar over billets has continuously narrowed, with processing premiums significantly declining, further squeezing profit margins in the long product segment. Meanwhile, sheet and plate products face more anti-dumping barriers, creating an opportunity for billet exports.

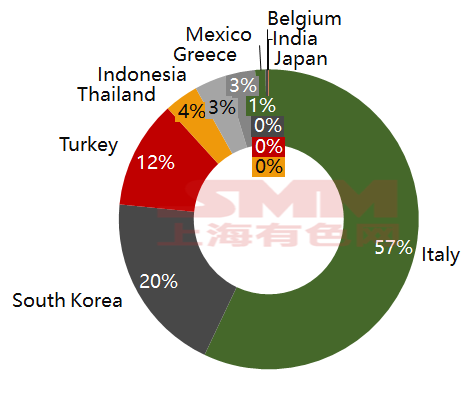

■ Slab Exports Have Fewer Destinations, Italy Accounts for Half

Figure 4: Regional Distribution of China's Slab Exports, January-August 2025

Data source: General Administration of Customs

Specifically, looking at exports by country for different varieties over the first eight months, slab exports went to only 10 destinations. Italy was the largest destination for slab exports, with a volume of 530,700 mt, accounting for 57.04%. South Korea was the second-largest destination, with 181,800 mt, accounting for 19.55%. Turkey ranked third, with 108,400 mt, accounting for 11.65%.

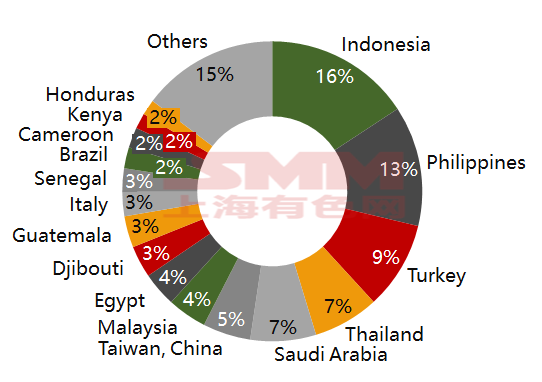

■ Indonesia Is the Largest Destination for China's Billet Exports, Accounting for 16%

Figure 5: Regional Distribution of China's Billet Exports, January-August 2025

Data source: General Administration of Customs

Billet export destinations are more diverse. Indonesia was the largest destination, with exports of 1.2882 million mt from January to August 2025, accounting for 15.73%. The Philippines was the second-largest destination, with 1.0626 million mt, accounting for 12.98%. Turkey was the third-largest destination for billet exports, with 775,200 mt, accounting for 9.47%. Destinations ranking fourth to tenth were Thailand, Saudi Arabia, Taiwan China, Malaysia, Egypt, Djibouti, and Guatemala.

■ Future Direction of Steel Billet Exports

On June 25, 2025, Jiang Wei, Deputy Secretary of the Party Committee, Vice Chairman, and Secretary General of the China Iron and Steel Association (CISA), stated at the Green and Low-Carbon Development Seminar that billet exports in the first four months of 2025 had already exceeded the total for the entire year of 2023, which to some extent drove up ore prices. As a semi-finished product, the surge in billet exports wastes domestic abundant deep-processing capacity, consumes domestic non-renewable energy and materials, leaves behind pollutants and carbon emissions, hinders the upgrading of the steel industry, and intensifies low-level market competition. The association has proposed suggestions to relevant national ministries to restrict billet exports.

In the long term, billet exports indeed have adverse effects on the development of China's steel industry. However, in the short term, there seems to be some rationale: insufficient domestic demand puts pressure on steel mills' sales, while anti-dumping friction against sheet and plate products intensifies. Although billet export prices no longer match rebar prices as they did last year, "increasing billet exports" appears to be an important way to alleviate pressure.

Simultaneously, anti-dumping investigations against billets are also increasing. For example, in June this year, Pakistan initiated a sunset review anti-dumping investigation on Chinese continuous casting billet products, and in September, Egypt initiated a safeguard investigation on imported steel billets. If the volume of domestic billets going overseas increases again, they may face more anti-dumping investigations, putting pressure on the sustainable development of billet exports. Balancing the domestic supply-demand pattern and increasing exports of high-end billets is the correct path forward. *This report is an original work and/or compilation created by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"). SMM legally owns the copyright, which is protected by the Copyright Law of the People's Republic of China and other applicable laws, regulations, and international treaties. Without written permission, it is prohibited to reproduce, modify, sell, transfer, display, translate, compile, disseminate, or disclose the above content to any third party in any other form, or permit any third party to use it. Otherwise, once discovered, SMM will take legal action to pursue liability for infringement, including but not limited to demanding compensation for breach of contract, restitution of unjust enrichment, and compensation for direct and indirect economic losses.

The content contained in this report, including but not limited to information, articles, data, charts, images, sounds, videos, logos, advertisements, trademarks, trade names, domain names, layout designs, and any or all information, is protected by the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, the Anti-Unfair Competition Law of the People's Republic of China, and other applicable laws, regulations, and international treaties concerning copyright, trademark rights, domain name rights, commercial data information rights, and other legal rights. It is owned or held by SMM and its relevant rights holders. Without written permission, no institution or individual may reproduce, modify, use, sell, transfer, display, translate, compile, disseminate, or disclose the above content to any third party in any other form, or permit any third party to use it. Otherwise, once discovered, SMM will take legal action to pursue liability for infringement, including but not limited to demanding compensation for breach of contract, restitution of unjust enrichment, and compensation for direct and indirect economic losses. The views in this report are based on information collected from the market and comprehensive evaluations by the SMM research team. The information provided in the report is for reference only, and users assume all risks. This report does not constitute direct investment research advice. Clients should make decisions cautiously and not use this report to replace their independent judgment. Any decisions made by clients are unrelated to SMM. Additionally, SMM is not responsible for any related losses or liabilities resulting from unauthorized or illegal use of the views in this report. SMM reserves the right to amend and provide the final interpretation of the terms of this statement.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)